Anchor: introduction

Education is our history.

WCTFCU was founded by Teachers in 1934. We are rooted in education. We continue to be committed to empower our members for financial success!

At WCTFCU, we’re here for every financial step you take. We’ll help you buy your first car, finance your home, prepare your children for their financial future and help improve your credit score all while giving you the tools to build financial wellness along the way.

Anchor: quicklinks

Make informed decisions about paying for college and managing your money.

- Articles, Videos and Webinars

- Interactive Modules

- What makes up a good credit score?

- How do you build good credit?

- Learn the steps you need to take to build a strong financial foundation.

What’s the best way to handle a credit card?

Learn the foundation here.

Students/Young Adults

Anchor: students

Savings Accounts

The foundation to building a solid financial future. Start earning today while you save for tomorrow.

- Members 17 and under earn a higher dividend rate with our Head Start Savings Accounts.

- Members 18 and older will open a Regular Savings Account.

Checking Accounts

Learn how to manage your money right from the start.

- No Minimum balance, No Monthly fee.

- A WCTFCU Visa Debit Card

- Download our fraud protection app for your card. Monitor spending habits and track purchases.

- Free Mobile and Online banking for easy access to manage your accounts.

- Set up Account Alerts to know when money is moving in and out.

- Mobile Check Deposit

- Direct deposit for your first paycheck

- eStatements (online copies of your monthly statements)

College Bound Students

For the next phase of your financial life.

- Scholarship opportunities are available every spring for WCTFCU Members graduating high school.

- Student Loans for Undergraduates and Graduates.

- Questions about how to finance College? Get the answers here.

- Financial Wellness for College. We have partnered with iGrad to offer financial education tools to help you navigate how to responsibly pay for school and manage your money.

Free Credit Score & Credit Reports

Anchor: free-credit

SavvyMoney

WCTFCU has partnered with SavvyMoney to offer Credit Union Members free access to their credit score, credit report, personalized money saving offers, tips on how to improve your score and more!

This free credit reporting tool can be accessed through online and mobile banking.

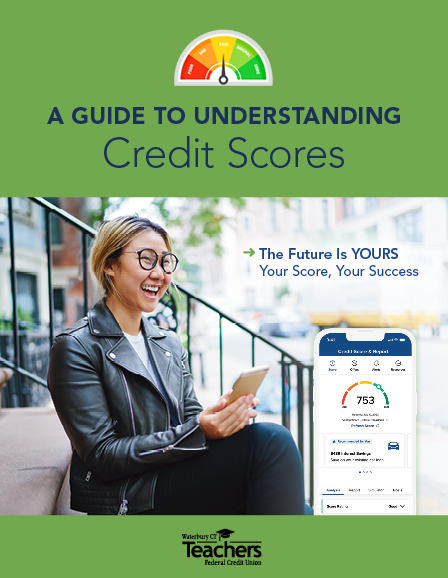

Guide to Understanding Credit Scores

Click on the booklet cover below to get the breakdown on what makes up your Credit Score.

What is a Credit Score?

A credit score is a three-digit number calculated to indicate your credit worthiness. The higher the score, the more credit worthy you are to a lender.

A credit score is calculated from information in your credit report and considers whether you have been making on-time payments, your revolving debt use, length of your payment history, as well as other factors.

It is important to know that your score does not take your age, income, employment, marital status, or your bank account balances into account.

What is a Credit Report?

Credit reports are composed of the credit-related data a credit reporting company has gathered about consumers from different sources. Credit reports include records of mortgage payments, credit card balances, credit card payments, auto loan payments and credit inquiries. It may also include accounts that have gone into collections, public records, and other information from government sources.

Credit reports include the following about your debt accounts:

- A list of companies that have given you credit or loans

- The total amount for each loan or credit limit for each credit card

- How often you paid your credit or loans on time, and the amount you have paid

Credit reports may also include:

- Companies that, upon receiving a loan application from you, have seen your credit report to evaluate your credit worthiness in the last 2 years

- Your address(es)

- Your employers

- Other details of public record

How do I improve my Credit Score?

There are several ways to improve your credit score. Here is some general advice:

- Pay your bills on time. How promptly you pay your bills has the strongest influence on your credit score.

- Apply for credit only when you need it. Do not open too many accounts too frequently. And avoid opening multiple accounts within a short time span.

- Keep your outstanding balances low. A good rule of thumb? Keep balances below 30 percent of the credit limit on each of your revolving accounts.

- Reduce your total debt. It is not necessarily bad to owe some money. But it is not good to owe too much money. Consider paying down some of your outstanding loans.

- Build up a credit history. Maintaining a timely payment history for a mix of accounts (e.g. credit cards, auto, mortgage) over a longer period can improve your score.

Life Stages

Anchor: life-stages

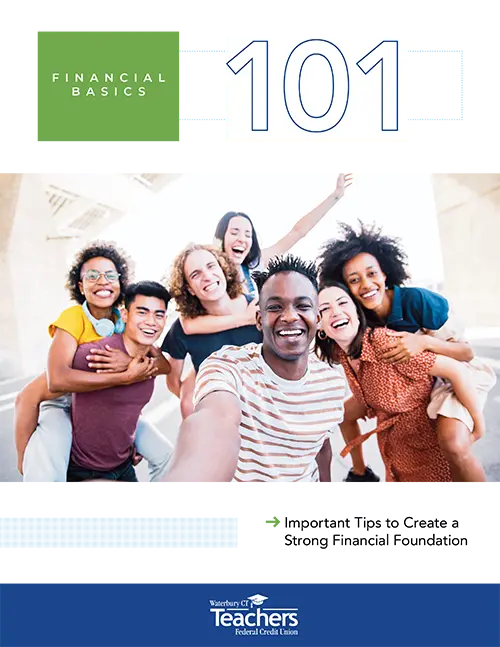

Financial Basics 101

Click on the booklet cover below for smart money tips on creating a strong financial foundation!

Buying your first car?

Here are a few tips to guide you on the road to success.

LEARN THE LINGO:

Auto Buying & Financing Terms

- Annual Percentage Rate: Commonly abbreviated as APR, this is the interest rate on a loan. It is also sometimes referred to as a finance rate.

- Dealer Incentives: These are special offers designed to encourage consumers to purchase a vehicle. Common incentives include cash rebates and low APR financing.

- Down Payment: This is the portion of money that you pay up front for a vehicle purchase.

- Monroney Sticker: This is the price tag sticker found on the windows of new cars. This document lists vehicle information such as the base price and standard features.

- MSRP: This acronym stands for Manufacturer’s Suggested Retail Price. It is the amount that is listed as the base price on vehicles’ Monroney stickers.

- Rebate: Designed to increase new-vehicle sales, rebates may be offered in the form of a price reduction or as a refund by mail upon completion of the sale.

- Term: This refers to a loan's length of time.

- VIN: A VIN (vehicle identification number) is a unique, 17-character code that identifies each specific motor vehicle in the United States.

Know the True Cost of Car Ownership

Trying to determine how much you can afford to spend on your vehicle purchase? When doing your calculations and reviewing your budget, keep in mind that the cost of car ownership goes far beyond a vehicle’s sticker price. Additional expenses include:

- Purchasing Fees: These include your taxes, tags and title, and can average around $1,000.

- Finance Charges: If you take out a loan to pay for your car, you’ll have to make monthly payments plus interest to pay it back.

- Insurance: Young and inexperienced drivers can be expensive to insure. Annual insurance cost averages range from $1,000 to $3,000.

- Maintenance and Repairs: The more you drive, the more upkeep your car will need, including oil changes and new tires. There are miscellaneous costs to consider as well, like parking fees and car washes.

- Fuel: Annual fuel costs can average close to $1,000 or more, depending on your car’s fuel efficiency and how much you drive.

- Depreciation: It’s the largest cost of owning a car. In five years, your car will be worth about 65% less than when you bought it.

Take the Wheel & Drive Home a Deal

When you’re ready to move forward with your purchase, follow these steps to help create a positive and affordable outcome.

- Know your credit score.

- Get pre-approved for financing. With a pre-approved loan, you know your maximum spending limit giving you negotiating power at the dealership.

- Do your Research: Informed shoppers are smart shoppers. Assess your needs. Do your homework on new and used car models and prices.

- Watch for Add-ons. Before signing the final contract, ask the dealer to explain each item. If there are charges you’re not comfortable with, don’t be afraid to point them out.

Steps to Buying a Home

Becoming a homeowner is a major decision, whether it is your first or forever home. Understanding these key steps will prepare you for the home-buying journey and help provide you peace of mind during the process.

Know Your Credit Score

The first step is to check your credit report to see where your credit stands and if anything needs to be addressed to improve it.

You can get your free credit report through your credit union by enrolling in SavvyMoney within online banking.

Your credit score will largely determine the terms of your mortgage. If your credit score is lower than you’d like due to missed payments or maxed-out credit cards, it’s in your best interest to put off purchasing a home until your credit score rises.

Organize Your Finances

Once you know your credit score, you need to take an honest look at your monthly income versus expenses and identify areas to save money, consolidate or do without.

Account for everything that your money goes to, including utilities, food, car payments and maintenance, student loan debt, clothing, childcare and kid’s activities, entertainment, retirement savings and any other areas.

Determine How Much Home You Can Afford

After organizing your finances and determining how much of your income can reasonably go toward your monthly mortgage payment, it’s time to calculate how much of a home you can afford.

Realize that there will also be up-front costs such as money needed for a down payment, closing costs and moving expenses and possibly new furnishings.

Save for added expenses

Buying a home usually requires saving money for a down payment, closing costs, moving expenses, new household utilities, new furnishings to name a few. Other things to consider are the costs for home inspections, upgrades to your new home, homeowner’s association costs (if any) and related costs.

Keep in mind it’s also good practice to have an emergency fund that can cover up to 6 months of living expenses, on top of all these other costs.

Financing Options

VIDEO SHORT: What is a Mortgage?

Before beginning your house hunt, it’s a good idea to get pre-qualified or pre-approved for a mortgage. Doing so will give you an idea how much you can afford to spend so you won’t waste your time looking at houses that are out of your price range. Keep in mind, though, that pre-qualifications and pre-approvals are two very different things:

- Getting PRE-QUALIFIED simply means that a lender has provided you with an estimate of the mortgage amount you will likely qualify for. If you choose to purchase a home, you will still have to go through the actual mortgage application process at that time.

- Getting PRE-APPROVED requires you to provide a lender with paperwork so they can verify your income, credit, etc. If that lender does decide to pre-approve you for a mortgage, it essentially means you are guaranteed to get a loan up to a specified amount (assuming no major financial changes occur) for a limited period of time.

When It Comes To Mortgages, One Size Does Not Fit All.

Numerous options and programs exist with different terms, features and benefits to suit various buyers. Be a well-informed consumer by familiarizing yourself with these common mortgage types:

Conventional/Fixed- Rate Mortgage:

A fixed-rate mortgage features an interest rate that remains constant throughout the term of the loan. Most fixed-rate mortgages come with a term of either 15 or 30 years.

Adjustable-Rate Mortgage (ARM):

Adjustable-rate mortgages typically start with a lower rate than fixed-rate mortgages, but after a few years the rate can begin to rise and will fluctuate periodically.

VA (Veterans Affairs) Loans:

VA loans offer up to 100% financing for military members and their families.

FHA (Federal Housing Administration) Loans:

FHA loans can help buyers receive financing even if they may not otherwise qualify for a mortgage. The FHA insures the lender for the mortgage amount – removing the risk associated with the borrower.

USDA (United States Department of Agriculture) Rural Development Loans:

These loans are available to rural residents who meet certain requirements, including the inability to be approved for traditional financing.

Balloon Loans:

A balloon loan is a mortgage in which a larger-than-normal outstanding balance must be paid at the end of the term.

Interest-Only Loans:

These loans offer borrowers a period of time when they pay interest only on their mortgage. (During the interest-only term, the borrower does not build any equity.) Once the interest-only term ends, the borrower starts to pay off the principal as well.

Selecting a Realtor

Select a Real Estate agent who thoroughly understands your housing needs such as type of home design, location, and price range. A good agent should be able to advocate hard for your offer during negotiations with the seller.

WCTFCU Mortgage Loans

Saving for Retirement

Investing early and often is a key factor when it comes to retirement planning. While it may be tempting to put off saving, research shows that beginning to invest in your twenties gives you the best retirement prospects later in life.

Start investing early. If you started investing $100 per month from age 25 to 35 and you earned an average of 5% per year. You’ll end up with way more at retirement age than if you started at age 35 and invested that same $100 a month all the way from age 35 to 60.

Dollar cost averaging is a strategy that can make it easier to deal with uncertain markets by making purchases automatic. It also supports an investor's effort to invest regularly.

Instead of investing a lump sum all at once, you can invest a smaller consistent amount at set intervals, like once a month, once a paycheck or every Tuesday.

This will average out your cost, so you can stop worrying about day-to-day fluctuations in your investment, and look at the big picture!

Concentrated Risk

The more concentrated your investments are in a certain company, market segment or asset class, the higher your risk of steep losses.

Instead, you want to build a diversified investment portfolio that spans different companies and industries, and includes a variety of different assets like stocks, bonds, index funds, real estate and more.

Financial Planning

Plan for your future.

The earlier you start planning for your retirement, the better.

Meet with a financial planner to map out your strategy for a successful financial future.

WCTFCU Members can make an appointment to meet with a financial advisor at Egidio Lennon Wealth Management LLC. Call today for a free, no obligation personal consultation.

Understanding Credit Cards

Anchor: understanding

Leave Some Room

- A credit limit is the total amount of money that can be charged to a credit card, including purchases, interest charges and fees. Keep tabs on how much room you have, and never max out your cards.

- In order to build up a good credit history, you want to be using 30% or less of your total credit. Keeping your utilization rate low will also help prevent your credit card debt from piling up faster than you can pay it off.

- Avoid maxing out your credit cards. Did you know that if your total utilization across all cards goes over 30%, it’s likely to hurt your credit score?

Pay In Full On Time

- When you have a credit card, it can be tempting to spend, spend, spend! Realize that it is a loan and you have to pay back every purchase you make. Try to save up ahead of time so you have the money set aside to pay the bill in full when it comes.

- The key to a successful relationship with your credit card is to pay it in full, and on time In addition, make sure to allow extra time for your payment to process!

Review Your Statement

It’s important to check your credit card statement every month. A credit card statement is a summary of how you've used your card for a billing period. It's important to read your statement carefully to spot any unauthorized charges or billing errors.

Manage Debt

Anchor: manage

Struggling With Debt?

With a little guidance and some elbow grease, your debt doesn’t have to define you. A debt-free future is possible.

Need a better strategy to pay off debt?

It helps to look at your monthly budget and make a debt repayment plan. If you can, pay more than the monthly minimum to pay down your principal balance quicker, and if you receive any financial windfalls, use them to pay off debt rather than treating them as spending money.

Just don’t touch your emergency fund. Without it, one bad turn could make your debt problems even worse.

Snowball vs. Avalanche Method

There are two popular methods used to paying down debt. The Snowball method pays off the lowest balance first, then moves on to the next lowest balance until you’re out of debt.

The Avalanche method starts with the balance that has the highest interest rate, then moves on to the next highest rate until you pay everything off.

The Avalanche method will save you more money in the long run, but it really comes down to which strategy will motivate you to reach the goal of being debt-free!

Debt Consolidation

If you are carrying expensive consumer debt including credit card balances and high-interest loans, you may consider a consolidation loan.

This is a form of debt refinancing that entails taking out one loan to pay off other smaller loans.

By consolidating your debt, you pack a bunch of smaller debts into one loan with a lower interest rate and only one payment. This will save you money and help you get back on the path to being debt-free.

Things You Should Know

Anchor: things

You Can “Buy Now, Pay Later,” But Should You?

Is there a purchase you want – and you want it now? Buy Now, Pay Later (BNPL) programs can be a convenient option for those who need to make a purchase but don’t have the necessary funds to do so. Knowing these programs are at your disposal can be helpful when you’re short on cash, but should you really use them?

As Buy Now, Pay Later programs rise in popularity, there’s no denying these programs are effortless, allowing consumers to purchase items of immediate need, like medical equipment not covered by insurance. For those with unsteady income, these programs can also make expenses more manageable in between paychecks.

Although these programs have their upsides, they must be used with care. If you’re not careful, Buy Now, Pay Later programs can be detrimental to your finances and credit.

Here’s What to Know:

Buy Now, Pay Later programs are essentially a point-of-sale loan, available online and even in some stores. For the avid online shopper, you may have noticed the BNPL button at online checkout with each retailer highlighting which Buy Now, Pay Later programs they offer. Common ones include Klarna®, AfterPay, Affirm and PayPal®’s Pay in 4.

To use a BNPL program, simply download the app of your desired program. The app will conduct a soft credit check – that’s right, there’s no hard-pull credit check – then, once you’re approved by the app, it’s time to make your purchase. Just pay the standard upfront payment, which is usually a 25% deposit on the purchase (although it may vary by program). It’s that easy!

At the time of your upfront payment, the program will have you link your credit card, debit card or checking account so the app can collect payments. Oftentimes, three fixed installments are needed to pay the purchase off. However, these payment plans can vary based on the program, like with PayPal’s Pay in 4 program.

If you’re thinking Buy Now, Pay Later programs sound like a credit card, you’re not wrong. However, unlike a credit card, there are no interest charges or fees – unless you miss a payment.

Sounds convenient, right? But is it too convenient?

So, What’s the Catch?

When using a Buy Now, Pay Later program, it’s important to be informed to prevent irresponsible financial habits from developing. These programs can be advantageous, but they can also be a downward spiral to debt.

BNPL payments can add up quickly, especially if frequently used for purchases. Make sure the fixed installments are factored into your monthly budget because missed payments are usually heavily penalized. To avoid such consequences, BNPL programs should be earmarked only for necessary, urgent items, not shopping hauls or other impulsive purchases.

Although it may be tempting to skip over, read the Installment Agreement! Oftentimes, there are rules, restrictions, regulations and penalties that may influence your choice in using a Buy Now, Pay Later program. This is the area where these programs can get consumers if they are uninformed about the consequences of not paying on time, as well as other conditions of the program. A quick search of the BNPL program you’re looking to use can also be a great way to understand the deals and downfalls of each program, as they all vary slightly. One program may be a better fit for you than another.

For the savvy spender, Buy Now, Pay Later programs can be a promising payment option when used with care and in moderation. They are not made to be heavily relied upon but as occasional support from time to time.

Webinars

Anchor: webinars

Pre-Retirement Planning Webinar

For Teachers and Administrators

Saturday, April 25th l 9:00 a.m. - 11:00 a.m.

Presented by our partner; Egidio Lennon Wealth Management LLC

Related Pages

.svg?sfvrsn=540134e0_1)

Featured Rate

Mobile Banking - access on the go

Mobile Banking - access on the go

View your credit score.

Apply for a loan.

Check balances.

Make transfers.

Deposit Checks.

Pay bills.